Financial institutions have long leaned on cash incentives to drive new account openings and deposit growth, and for good reason. The promise of a cash bonus is an effective way to get consumers to start a conversation with an FI or consider switching. However, new data shows that the offer alone does not always give these accountholders a reason to stay long-term.

In March 2026, Vericast surveyed 1,000 U.S. adults to understand what consumers really think about cash incentives. The data shows that while incentives can open the door to new acquisition, building a lasting relationship requires more than the initial offer. To get the most out of incentive campaigns, FIs should consider retention planning as an equal part of the campaign development process.

How Incentives Land Depends on Who You’re Targeting

To understand how FIs can get the most out of cash incentive campaigns, it helps to start with what consumers actually think about them. When we asked consumers if they have ever switched financial institutions because of a promotional cash offer, one quarter (25%) said yes and stayed long-term. In contrast, 33% said they considered it but didn’t make the leap, and a near-equal share (34%) said they would not switch just for a bonus. This signals that offers can generate initial attention, but they’re only one of several factors consumers weigh when considering a new FI.

While 28% said they see bonus-driven incentives as a smart way to earn extra money, another 28% called them a short-term gimmick. This highlights the risk of relying on incentives in isolation. When offers appear disconnected from product value, brand strength, or a clear onboarding path, consumers appear more likely to dismiss them as transactional rather than trust-building.

Only 10% of respondents perceive these offer as capturing loyalty; 22% recognize them as a normal part of the banking competition.

These perceptions also vary across generations:

- Baby Boomers: 40% of respondents call bonuses a gimmick, and only 5% see them as a means for an FI to earn their loyalty

- Millennials: 33% of respondents view bonuses as a smart financial move, making them the most receptive of any generation

- Gen Z: 21% of respondents view a large cash offer as a sign of desperation, the highest of any generation

What this data tells us is that a one-size-fits-all incentive message may not resonate equally across all audiences. To help ensure fair treatment, these differences should be best understood as indicators of how to adjust messaging based on the segments you hope to reach—and not as a basis for limiting eligibility or access to offers.

Matching the Offer to the Audience

“The average cost of acquiring a new customer (cost per acquisition, or CPA) is now 69% higher than it was in 2019, jumping from $437 to $743.”

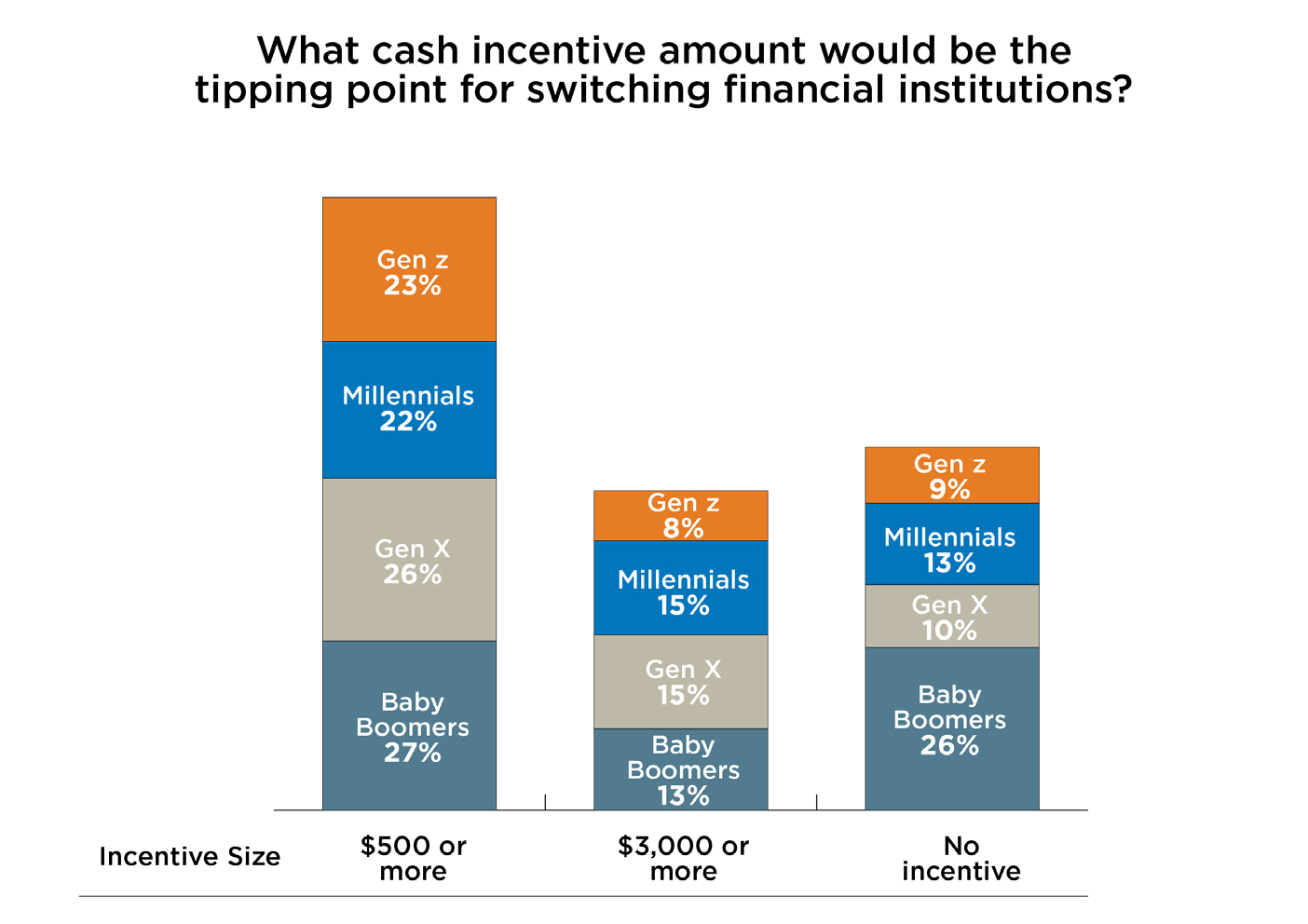

One in four (25%) of respondents stated that they would require at least $500 to switch FIs, and 32% need upwards of $1,000. At the same time, 15% say they would not switch for any amount, rising to 26% among Baby Boomers.

On the other end of the scale, Gen Z appears more responsive to lower thresholds, with 10% of respondents saying a $50 offer or more would be enough to switch FIs. But for this generation, larger offers don’t appear to move the needle by much. Only 8% said an offer of $3,000 or more would be their tipping point, compared to 13% of Baby Boomers and 15% of Gen X who said the same. These findings demonstrate varying perceptions of

incentives, which can be used to enhance messaging, personalization, and channel selection.

This can put FIs in a tricky spot where larger incentives increase acquisition costs without guaranteeing conversion. This is why it’s important to ensure that the offer is delivered in ways that are relevant and timely for consumers who may be open to switching, while maintaining consistent offer availability and eligibility across audiences.

This does not require constant changes to the incentive itself. Personalization should focus on how an offer is presented—such as messaging, creative treatment, channel selection, and onboarding experience. Institutions must, of course, implement personalization strategies consistent with fair banking and consumer protection principles.

Many FIs can see stronger results when they maintain a consistent core offer while personalizing how it’s framed and where it appears. Stability in the offer builds market clarity, while personalization in delivery ensures relevance across audiences.

When the Bonus Is the Same, Personalization and Trust Wins

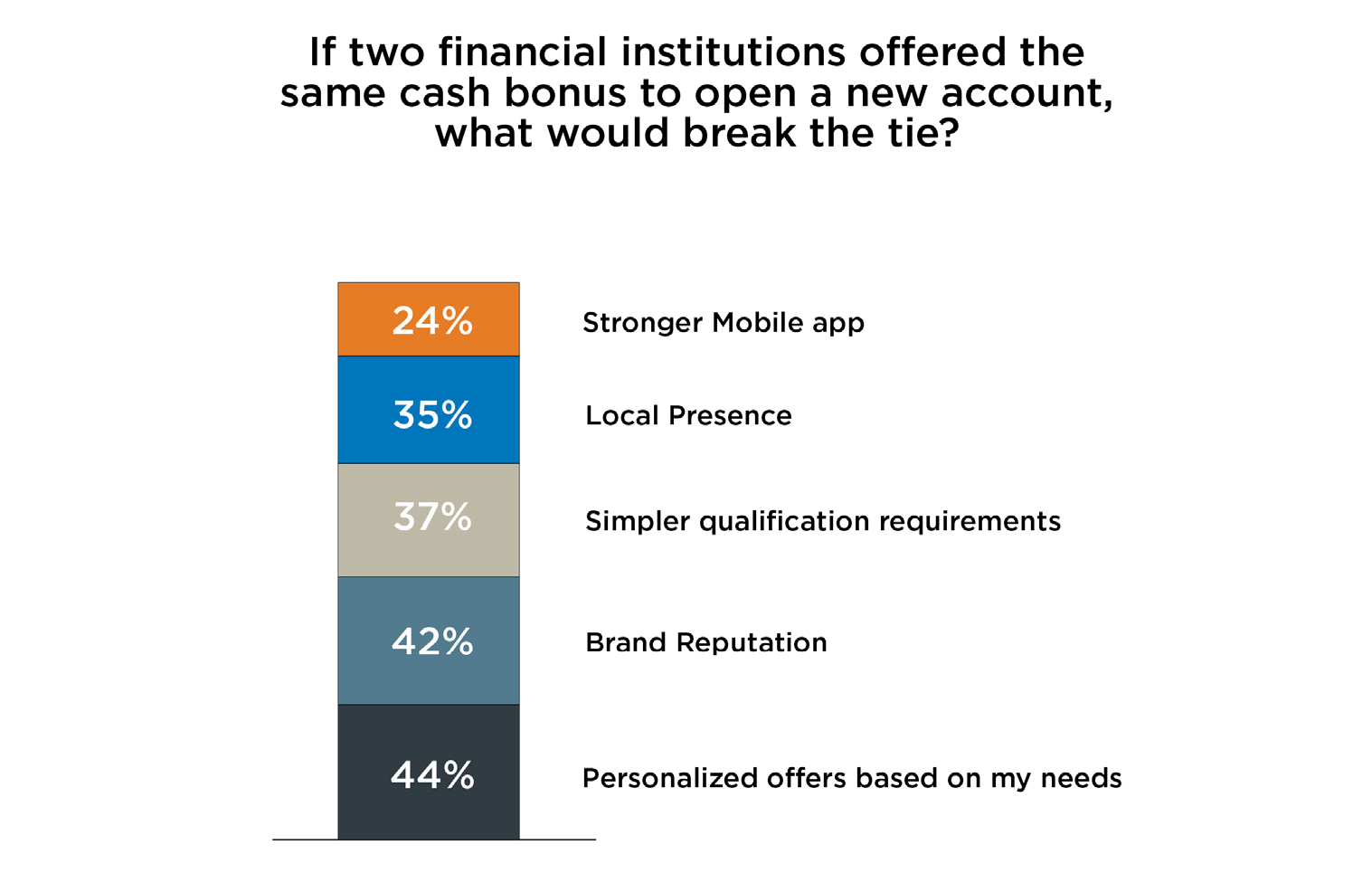

When presented with two identical cash offers, consumers appear to expand their evaluation criteria.

Based on Vericast’s survey data, personalized offers based on consumers’ needs ranked first at 44%, reflecting a preference for financial products and messaging tailored to consumers’ specific situation rather than a generic pitch. Brand reputation came in second at 42%, and local presence, whether the FI has branches or community ties in their area, ranked third at 35%. Among Baby Boomers, localization carried even more weight, with 50% of respondents citing it as a deciding factor in switching FIs in this scenario.

Relevance, trust, and community ties are often the deciding factor, especially when products and offers are similar. FIs that invest in building those capabilities are better positioned to win the account when the dollar amounts are equal.

Requirements Can Filter Intent

Vericast’s survey data shows that the structure of the offer matters, too. When asked whether multiple conditions – like direct deposit, debit card usage or a minimum balance – to receive the incentive would affect their likelihood to switch, 39% of respondents said it would deter them. On the other hand, 30% said it would increase their likelihood of switching and 31% said it would have no impact on them.

This shows that conditions or qualifications serve two different roles. For some, they create too much hassle. For others, they can signal a more meaningful, long-term banking relationship.

The takeaway is not to add more requirements, but to use these criteria thoughtfully and transparently, aligning with the account’s ongoing value rather than serving as barriers that could unintentionally exclude certain consumers. When qualifications are clearly connected to how an account delivers long-term value (such as direct deposit, debit usage, or rewards enrollment), they function less as barriers and more as early indicators of genuine intent. In this way, requirements, appropriately monitored, can strengthen retention without compromising conversion or disproportionately discouraging participation or access.

Account Opening Is Not the Finish Line

The challenge with any incentive program isn’t getting consumers in the door; it’s whether those acquired are driving long-term value. A cash offer can be effective at generating new account openings, but what those accounts are worth six months later is where the real return on an incentive campaign becomes clear.

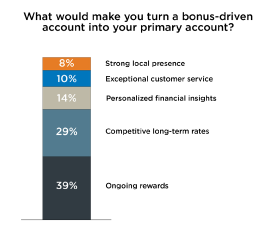

The good news is that, per Vericast survey data, consumers seem fairly clear about what it would take to make a bonus-driven account their primary one.

- 39% cite ongoing rewards

- 29% point to competitive long-term rates

- 14% cite personalized financial insights

- 10% point to exceptional customer service

- 8% cite strong local presence

Ongoing rewards ranked as the top driver for retention at 39% of respondents, and that finding holds steady across generations, with Boomers at 38%, Gen X at 42%, and Millennials at 43%. For consumers who opened an account for a bonus, a rewards program gives them a tangible reason to keep using it after the initial transaction is complete.

Competitive long-term rates came in second at 29%. For nearly a third of respondents, the decision to make an account primary comes down to whether the rates are worth staying for once the bonus is gone.

Personalized financial insights ranked third overall at 14%, but amongst Gen Z respondents that number climbs to 27%. The gap between 16% leaving after the bonus and 27% wanting personalized insights signals that the path to retaining younger customers comes from the level of insight an FI can provide as they navigate different financial milestones.

For FIs, these findings show a move from transactional activity to continuous value where ongoing relevance supports becoming the primary institution.

What Should FIs Do with This Data?

Cash incentives remain one of the most visible tools for driving conversations around account openings, but the data points to three things FIs need to consider to improve their chances of seeing better ROI: incentives are not one-size-fits-all, an incentive strategy without a retention plan is an expensive way to move money without building a relationship, and the foundation underneath the offer matters as much as the offer itself.

- Get precise before you get generous. Bigger bonuses do not appear to guarantee better returns, especially when a meaningful share of consumers say they would not switch regardless of the amount offered. Precision targeting can help FIs improve efficiency by tailoring messaging and channel strategy to consumer interests and behaviors, while ensuring that offers remain broadly and fairly available.

- Build a retention strategy before the bonus clears. Cash incentives are effective at opening accounts, but what seems to keep those accounts open is what the FI does next. Onboarding and engagement strategies that reflect what different segments need over time, whether that is ongoing rewards, competitive rates, or personalized financial guidance, are what turn a new account into a primary one.

- Personalize beyond the offer. When two institutions offer the same bonus, the incentive stops being the differentiator. Consumers choose based on who knows them better, whose brand they trust, and who feels like part of their community. FIs who invest in personalized marketing and a strong local presence are building the case for why a consumer should choose them before the bonus enters the conversation.

Our survey data doesn’t indicate that cash incentives are a waste of resources. Rather, it suggests that the offer gets attention, and then it’s up to an FI to maintain that interest by delivering long-term value that meets accountholders’ needs.

Curinos, “This Month in Retail Banking: Spending, Shopping and More”curinos.com/our-insights/this-month-in-retail-banking-spending-shopping-more/