Banks and credit unions are coming close to a crossroad that may force them to expend significant capital. What to do with the evolving purpose of the brick-and-mortar branch office?

Technology Takeover

The smartphone and robust mobile banking applications are dramatically changing the way consumers conduct their business. Gone are the days when account holders needed to head to a branch location to deposit a check, move money from one account to another, get current account balances, etc. etc. etc. All of that is now being accomplished with the help of that powerful little computer sitting in the palm of their hand.

According to a recent American Banker article:

- JPMorgan Chase said that 70 percent of the 400 million transactions completed through its tellers in 2016 could have been completed using its mobile app or another self-service channel.

- Bank of America is seeing declines in teller transactions at the rate of double-digit percentages over the past few years. Five years ago, 65 percent of customers’ deposits were made at a Bank of America teller window and 35 percent at the ATM. Today, half of all Bank of America deposits are made at the ATM, 20 percent on mobile devices and 30 percent with the help of tellers.

Downward Trend

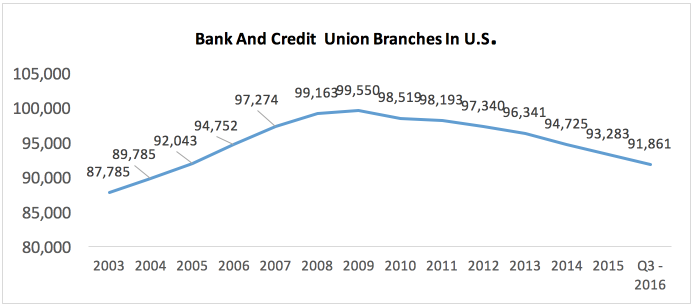

The chart below, from BankRegData.com, shows the decline in the number of bank and credit union branches in the U.S. It is likely that the downward trend will only accelerate as technology continues to drive changes in consumers’ banking behavior.

What Can Banks and Credit Unions Do?

So… what can you do about it?

You can differentiate your bank and credit union by changing the role of the branch. This is easier said than done, obviously, but the successful financial institution of the future will do this.

What do I mean by “changing the role of the branch?” Well, study after study points to the difficulties Americans have in managing their money. We need help getting from point A to point B financially. The financial institution that turns its branches into centers of information, where advice and consultation are proffered to account holders, will be recognized as an entity that truly wants to help consumers. So, while less and less transactions occur at the branch, more and more advice and consultation can take place instead.

Surely, this is a better approach to making the branch office relevant rather than turning it into a venue for yoga or coffee or art. Haven’t banks and credit unions had enough difficulty getting consumers to understand the breadth and depth of our product lines? Let’s not put Planet Fitness, Starbucks and the local art museum on the list of competitors.

>>Struggling to acquire new accounts? Grab the “5 Ways to Acquire New Accounts to Meet Your Annual Goals” tip sheet for extra advice.